- Markets Mirage

- Posts

- One week / one topic: Trading the tape

One week / one topic: Trading the tape

Everyone's feelin' pretty / It's hotter than July

Stefano Amato

February 02, 2026

What happened?

The first month of 2026 has come and gone, and we can safely say that the year has started out with a bang.

In almost every way you can think of, there have been plenty of market-moving developments:

Seismic changes to the post-WWII international order? Check

Runaway price action in many corners of the market? Check

Radical changes in the fiscal and monetary policy stance of major countries? Check

I could keep going, but frankly just trying to keep up has been utterly exhausting.

Past performance is not a guide to future performance. Data as of 30/01/2026

Resisting the siren song of ever-more-seducing grand narratives is quite difficult – Regional fortresses! Currency debasement! Run it hot! – not least because there is at least some truth to all of them… otherwise we wouldn’t be here, no?

In this environment, one’s survival instincts (at least mine) point to the supremacy of price above all else, because – while we do own in portfolios some of the best performing assets of the last few months – “the first principle is that you must not fool yourself—and you are the easiest person to fool”. (Richard Feynman)

In practical terms, I think it means taking a step back and observing the price action as if you were not a performer participant in this circus.

There are more than enough ringmasters, trapeze artists and clowns around… so let’s step out of the tent and aim for that ever-elusive – but enormously valuable – ‘view from nowhere’ indeed.

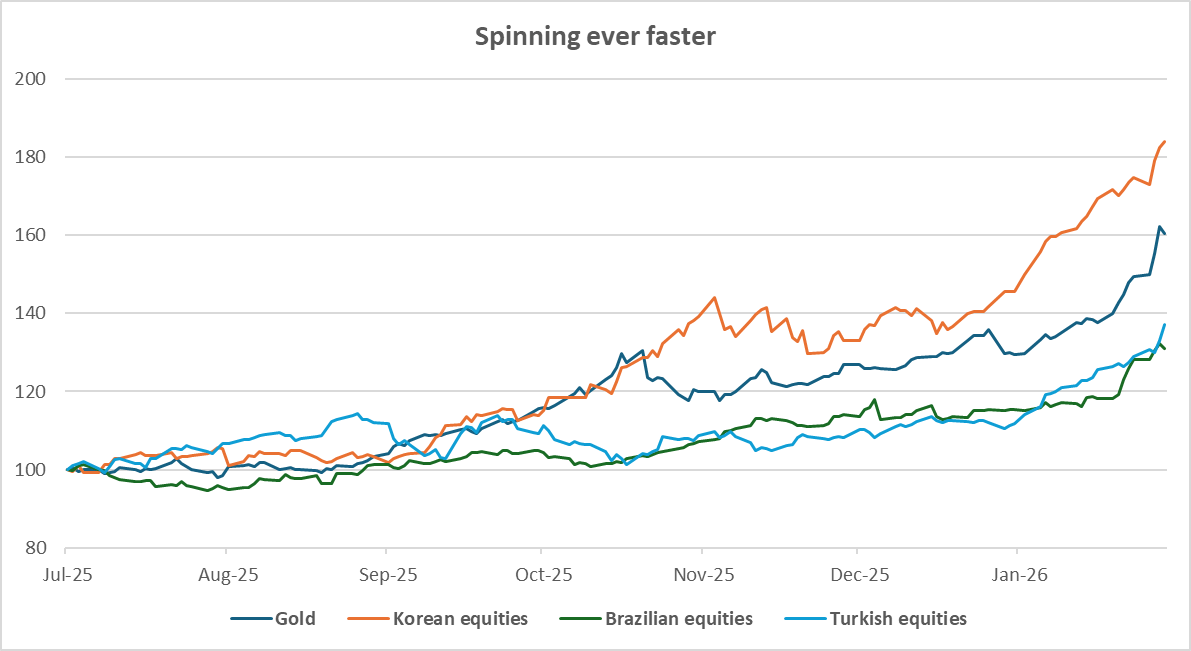

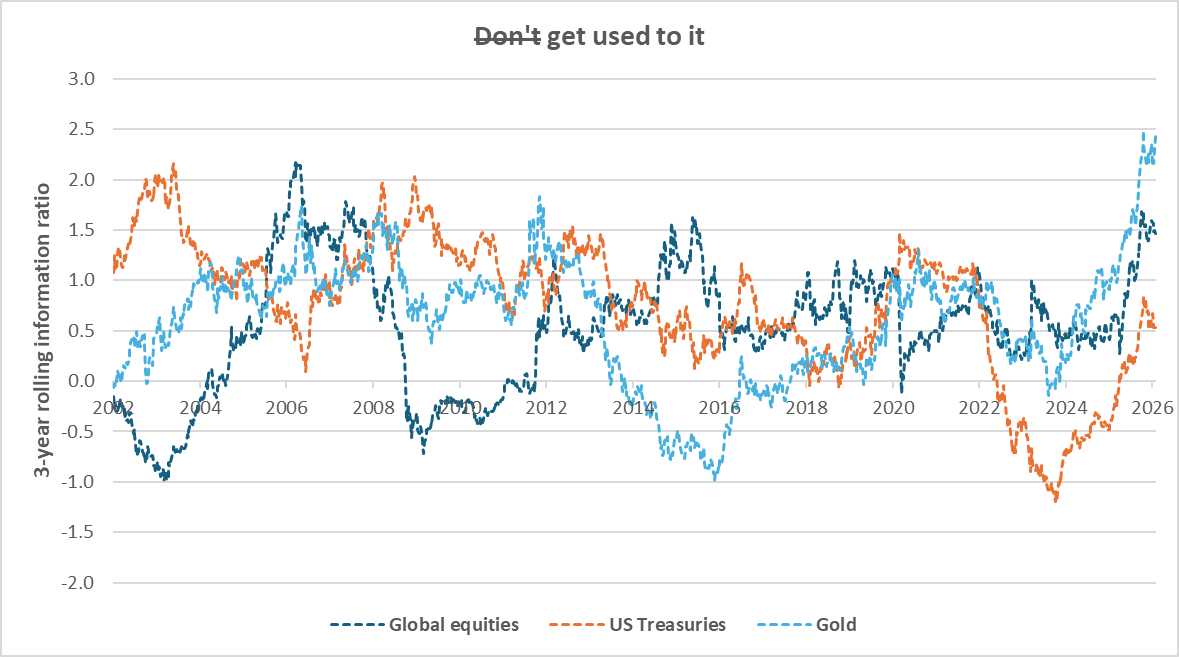

When engaging in this exercise, recent price action in my view points to a structural discontinuity.

After all, risk-adjusted returns for Equities and Gold have rarely been this good…

Past performance is not a guide to future performance. Data as of 30/01/2026

What to do, then?

Should you hold on to your conviction that time-tested investment principles will ultimately reassert themselves?

Or are you better off trying to change with the times?

Our observations

Fundamentals: As pointed out before, it increasingly feels like risk appetite is ultimately the (only?) fundamental that really matters. Collectively, we are very good at coming up with stories to justify almost anything… so why should runaway price action be an exception?

Price action: Being prone to sensationalism is looked down upon by many ‘fundamentals-oriented’ fund managers, and it’s easy to understand why. However, prices don’t care about your principles, and – once again – you fight momentum at your peril.

Investor beliefs: Are we increasingly ‘defining deviancy down’ as of late, or is there simply increased visibility about risk-seeking behavior in markets?

Past performance is not a guide to future performance. Data as of 30/01/2026

So what?

A friend with a stellar Wall Street career recently commented that ‘all the old school macro greats ultimately traded the tape’.

(i.e. focused on price action over fundamentals)

Indeed, there is ample testimony of this:

George Soros: “Markets are constantly in a state of uncertainty and flux, and money is made by discounting the obvious and betting on the unexpected.”

Paul Tudor Jones: “While I spend a significant amount of my time on analytics and collecting fundamental information, at the end of the day, I am a slave to the tape and proud of it.”

Stanley Druckenmiller: “I never use valuation to time the market… I use liquidity considerations and technical analysis for timing.”

Source: Dribble

While we don’t run an unconstrained leveraged macro fund, I think this is very relevant right now. (Also, I don’t have the presumption to think that I know better than these gentlemen!)

In practice, this means holding on to some of our best-performing holdings – Japanese, Brazilian and Turkish equities, plus a collection of various emerging market currencies – while retaining discipline by taking some profits on these positions, and keeping enough length so as to not get in the way of powerful price trends.

However, the question is much more difficult when it comes to our holdings in developed markets government bonds.

In the current fiscally expansive environment, these assets have increasingly behaved like ‘term premium risk’ as opposed to ‘risk-off hedges’.

Uncomfortably and perhaps also unwillingly, maintaining reasonable duration exposure in portfolios against the risk of unforeseeable deflationary shocks still seems sensible.

A balancing act, indeed.

After all, you can’t really have a circus without trapeze artists…

Mood music: Stevie Wonder – Master Blaster (Jammin’)

By popular demand, here is the One week / One topic playlist