- Markets Mirage

- Posts

- One week / one topic: Molecules

One week / one topic: Molecules

Let it burn

Stefano Amato

March 30, 2026

What happened?

Markets remain dominated by the Iran conflict and the associated energy shock, with attention now (finally) focused less on headlines and more on the risk of physical disruption to oil and refined product flows.

After all, at some point the reality of the energy supply shock has to move from traders’ screens to the real world – and you actually start to feel it.

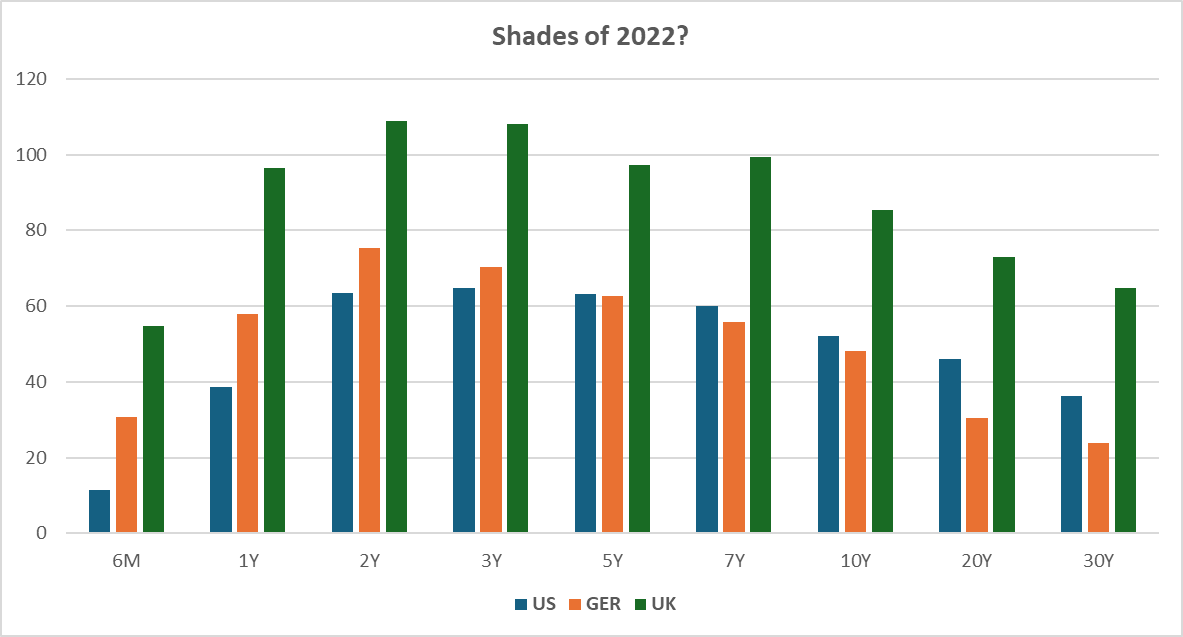

Rates markets reacted most forcefully, with a sharp hawkish repricing at the front end across G10 and parts of EM as investors and central banks alike remained sensitive to second‑round inflation risks after the scarring experience of 2022.

Yield moves in developed market bonds over the last month – below, in basis points – make this quite clear.

Source: Bloomberg. Data as of 27/03/2026

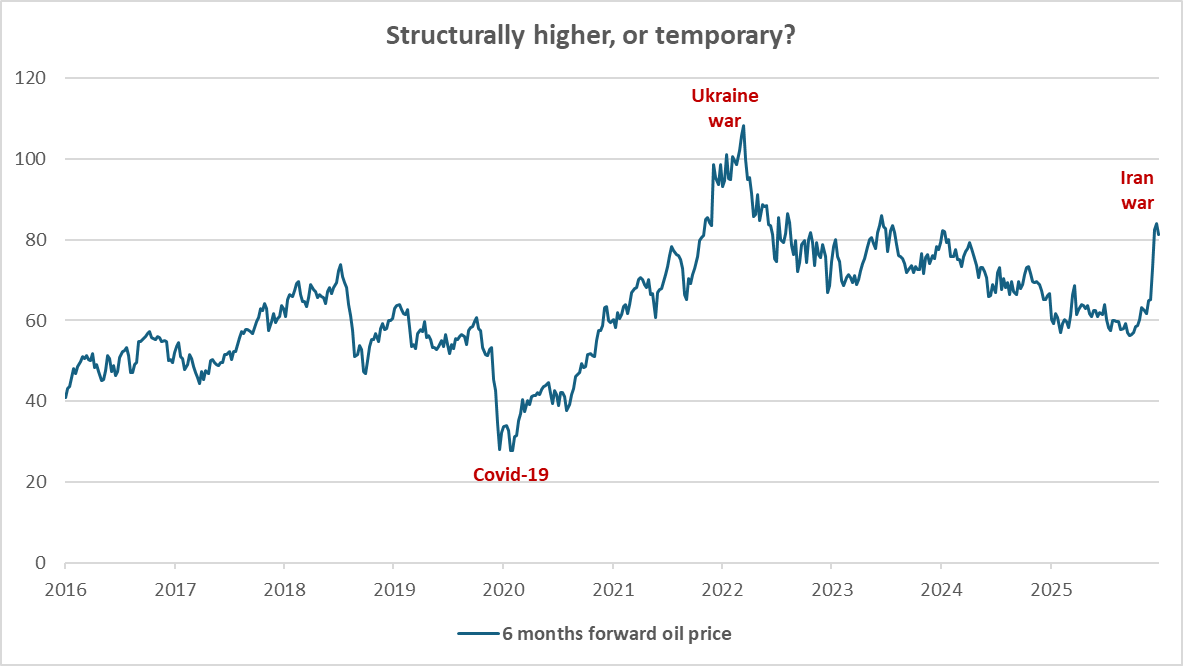

Even without a full closure of the Strait of Hormuz – the likelihood of which remains utterly unknowable, amid all the vagaries of Schrödinger-like negotiations between Iran and the US – the ever-more-credible threat of prolonged supply interruption has conclusively lifted oil’s floor and broadened inflation concerns beyond crude into transport, power and industrial inputs.

You can glue the teacup back together, but it’s never going to be the same.

Now that there is a precedent for closure of the Strait of Hormuz, the price of long-term oil most likely needs to be higher to reflect this risk.

Source: Bloomberg. Data as of 27/03/2026

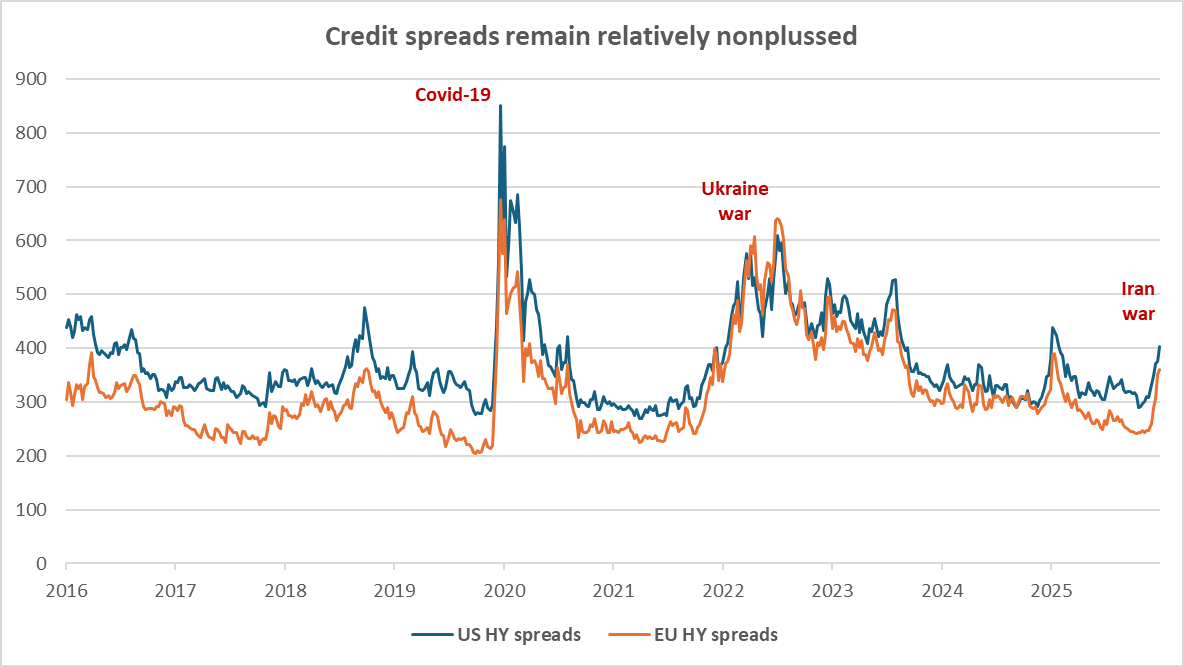

By contrast, equities (until recently) and credit have been more resilient, reflecting the view that growth damage is conditional on a prolonged or escalatory shock rather than the base case.

There is also visible dissonance at play, as some markets have perhaps been more discerning about pricing in the potential impact of recent events.

For example – while emerging market bonds increasingly reflect energy terms‑of‑trade differentiation – credit spreads remain pretty unperturbed.

Source: Bloomberg. Data as of 27/03/2026

What are we to do then, in the presence of a meaningful and utterly unpredictable source of uncertainty?

Our observations

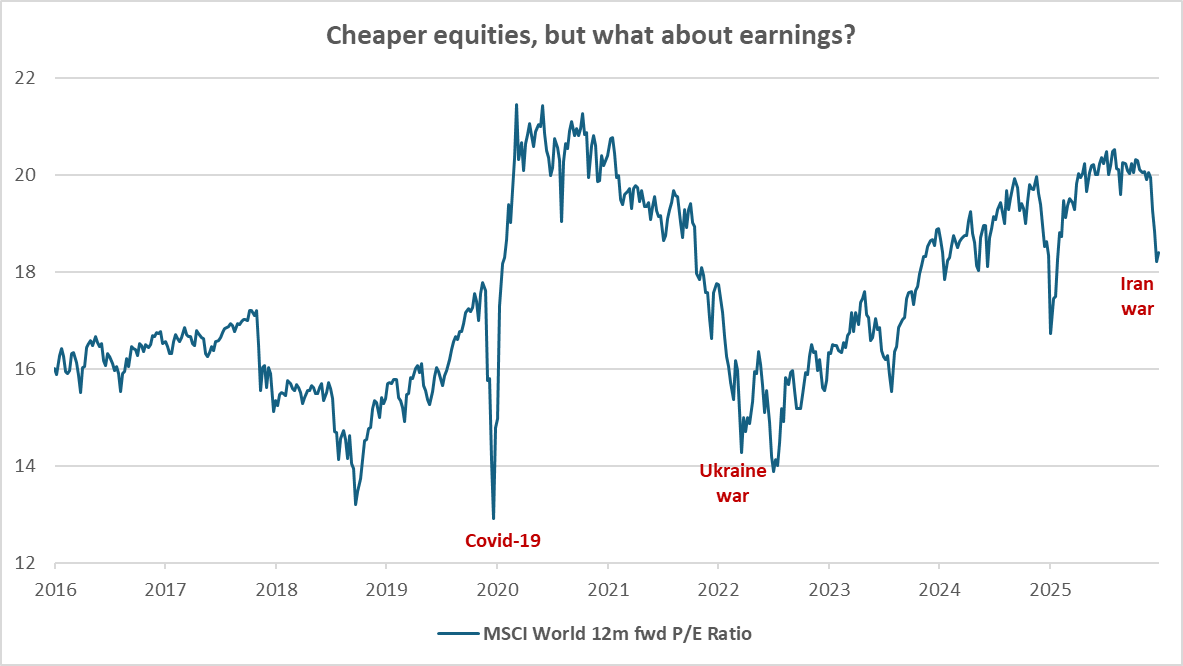

Fundamentals: Equities might well have repriced lower, but earnings estimates have not really been updated – mostly because people have no idea.

How confident can you be then that there is now an appropriate risk premium?

Price action: While there have been some relatively violent moves, in general we have not observed true panic across the board.

This might well change at any time of course, and ‘headline bingo’ dynamics look likely to persist.

Investor beliefs: Confusion, complacency, concern… take your pick.

Meanwhile, every day the underlying reality of continued disruption in the physical world becomes more likely to (finally) affect risk appetite.

Source: Bloomberg. Data as of 27/03/2026

So what?

Putting it all together, we are considering a tactical reduction in developed markets government bonds duration.

This would take the shape of rotating out of long‑dated government bonds and into the 5‑year part of the curve, with a preference for US and UK over Germany, which is also the segment that has repriced more violently over the last month.

The aim is to protect the portfolio against further upside pressure on yields if Iran‑related energy disruption keeps inflation risks elevated.

While we remain fully aware of how utterly unpredictable the situation is, this is more of a risk‑management move to lower sensitivity to yield spikes while retaining flexibility, and can be reversed quickly if the situation de‑escalates.

Mood music: Adele – Set Fire To The Rain

By popular demand, here is the One week / One topic playlist