- Markets Mirage

- Posts

- One week / one topic: Hormuz

One week / one topic: Hormuz

A million candles burning

Stefano Amato

March 09, 2026

What happened?

The US/Israel attack on Iran has quickly morphed into a regional conflict, with significant human toll already and increasingly unpredictable consequences.

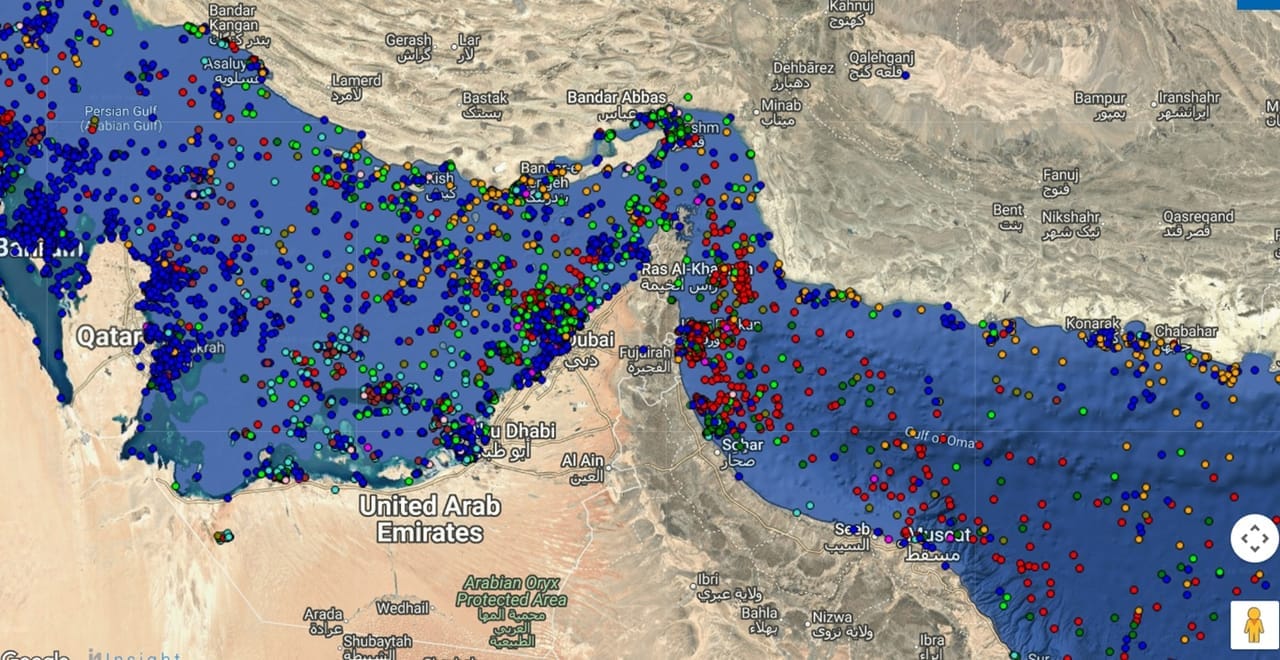

Meanwhile, traffic through the Strait of Hormuz – accountable for one-fifth of the world’s oil and liquified natural gas (LNG) traffic – has essentially stopped.

Source: seatrade-maritime.com

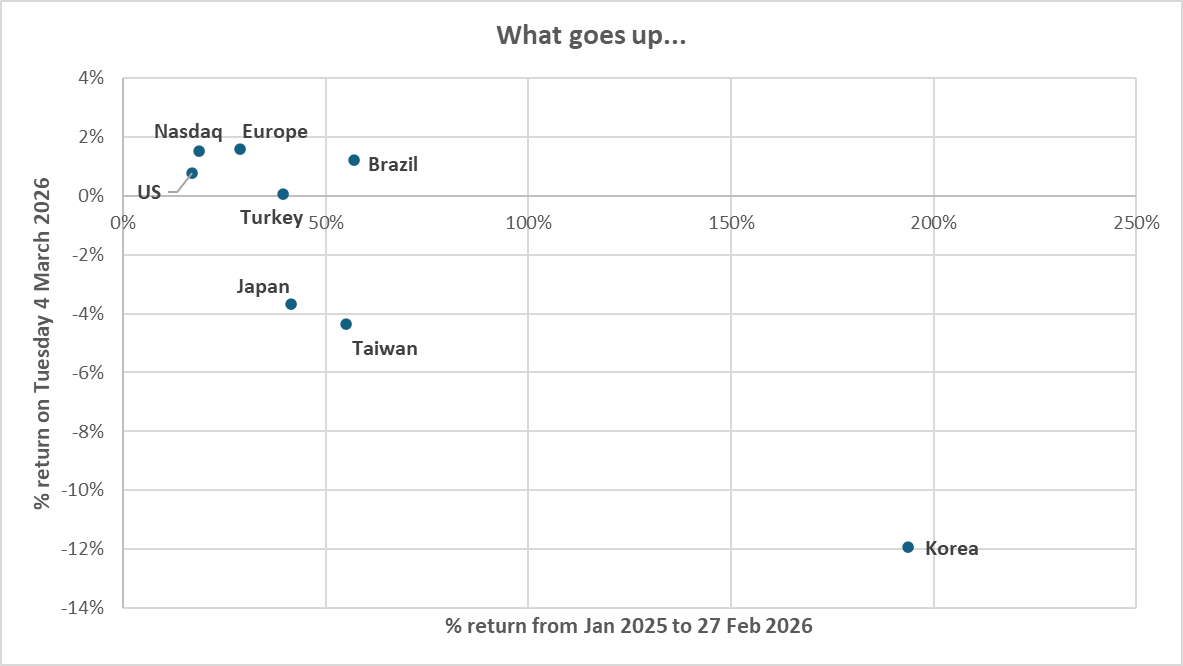

So far, the initial market reaction looks sharp but orderly.

Equities have seen recent winners reprice meaningfully lower, also as many of them (i.e. Asia) largely depend on imported energy.

On the other hand, US stocks have fared better as the country is far away from the war theatre and a large net energy exporter.

Source: Bloomberg. Data as of 06/03/2026. Past performance is not a guide to future performance.

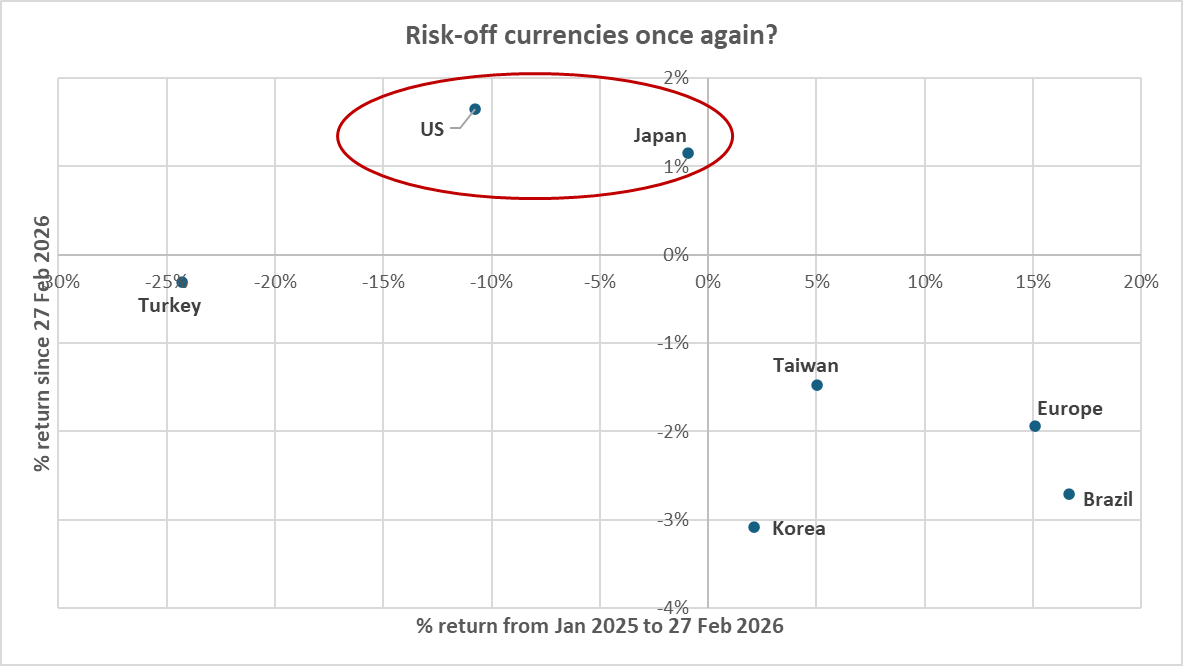

Currencies have also followed a similar pattern, a possible tell of liquidation / de-grossing dynamics.

At least for now, the US Dollar and the Yen have benefitted from what looks like a classic flight to safety.

Source: Bloomberg. Data as of 06/03/2026. Past performance is not a guide to future performance.

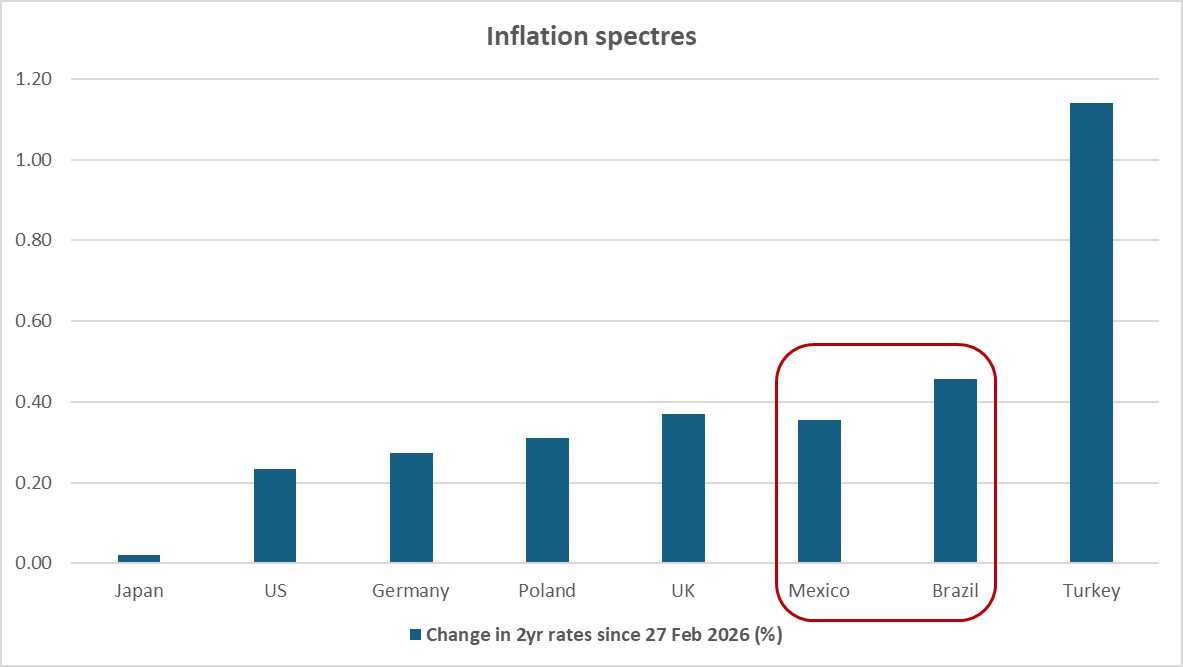

Government bonds have quickly priced in the inflationary impact of higher energy prices, perhaps also exposing pre-existing nervousness about price stability.

Brazil and, to an even larger extent, Mexico however stand out, as their vulnerability to higher energy prices should actually be lower than Poland, for example.

Source: Bloomberg. Data as of 06/03/2026

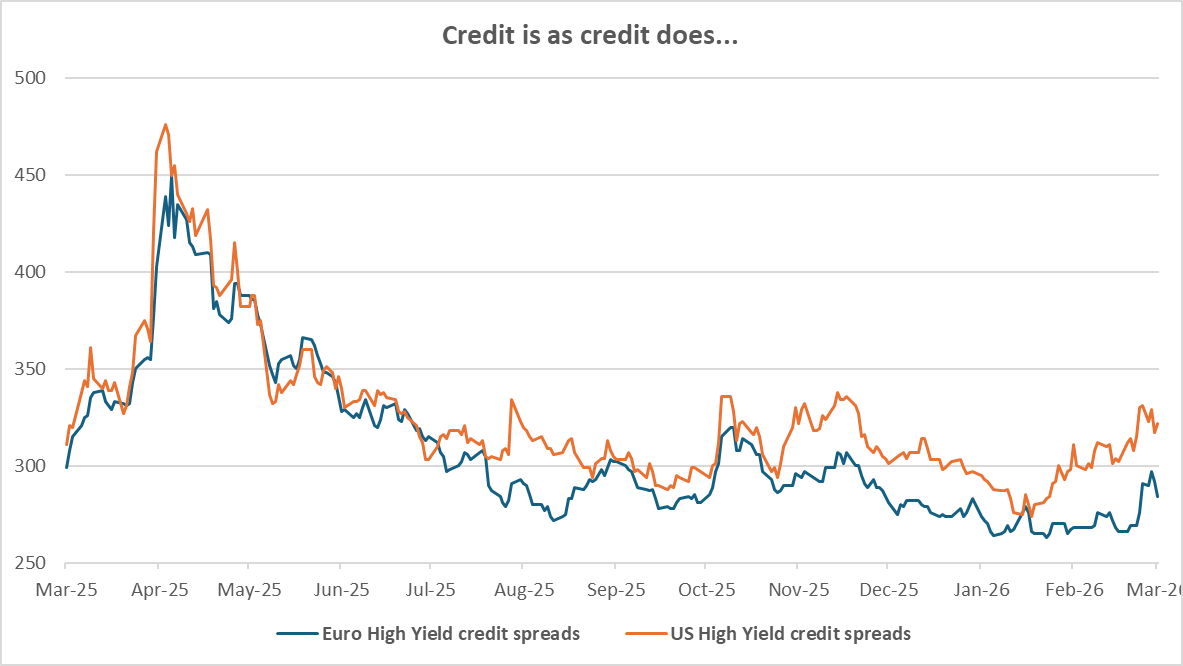

Credit spreads have been widening for some time, due to increasing concerns around private credit and AI capex funding.

It remains notable however how the reaction over the last week was relatively muted.

Source: Bloomberg. Data as of 06/03/2026

What to do then, in the middle of (yet another) meaningful shock to the system?

Our observations

Fundamentals: Markets seems to have rationally sorted through which assets are more (or less) vulnerable to the known risks at hand, and repriced them accordingly.

Also, the starting point for most of the equities complex were expensive valuations – and the moves so far have not meaningfully altered that picture.

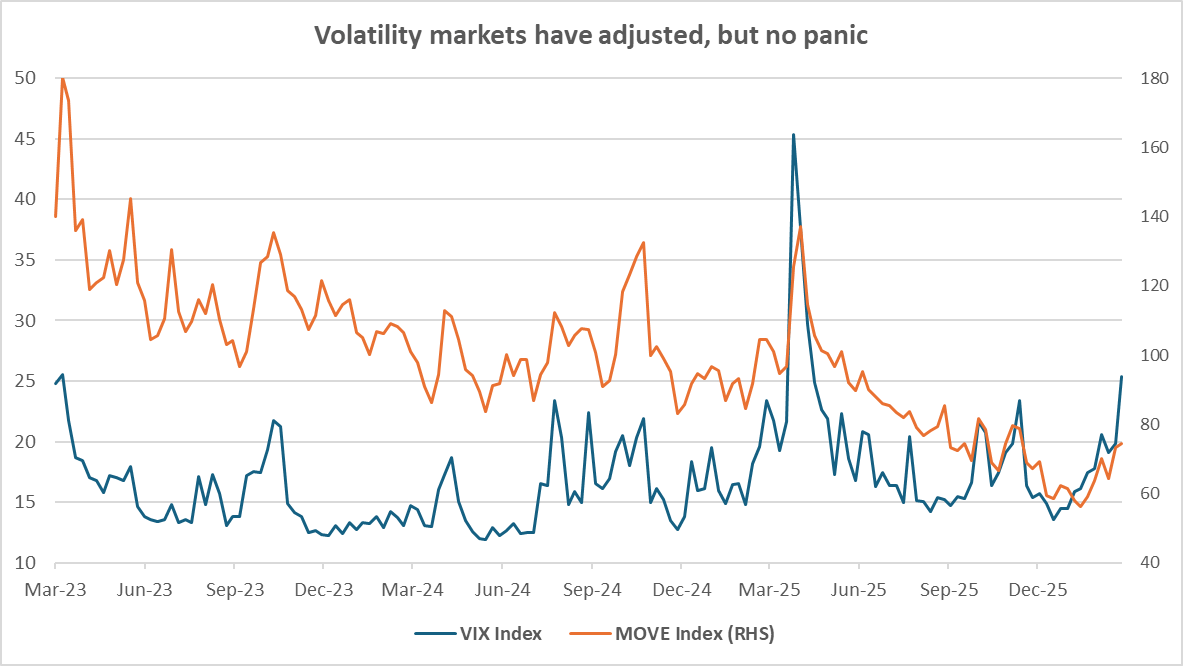

Price action: While some of the moves were extremely sharp (Korean stocks -18% over two sessions), the overall picture – if anything – still feels too calm given what’s potentially at stake?

Expected equity and rates volatility (below) have adjusted higher, but the move for now is not extreme.

Investor beliefs: Oil specialists argue that the impact is still underpriced, but on the other hand enough pain could ultimately lead to a negotiated outcome.

Managing the path is the task at hand then, with larger dislocations potentially offering opportunities at some point.

Source: Bloomberg. Data as of 06/03/2026

So what?

Putting it all together, it’s hard to identify any obvious required adjustments to portfolio positioning.

Also, there is a notable pattern of major events happening over the weekend, therefore adding gap risk between the Friday close and when markets reopen the following Monday.

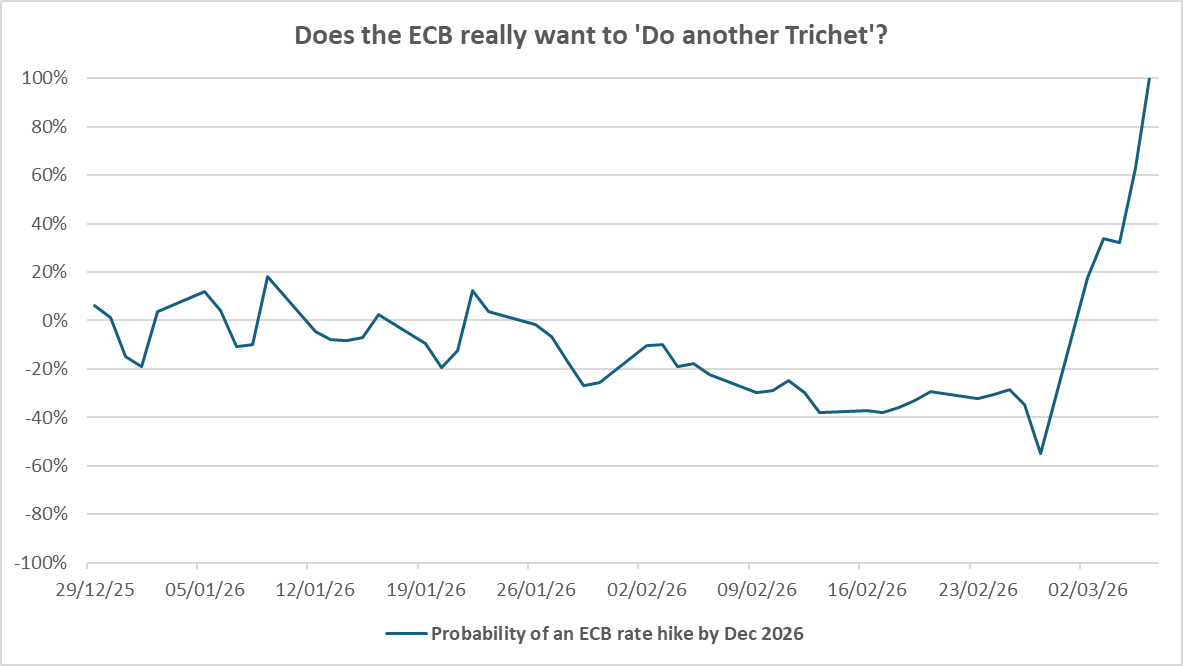

What stands out here is that European rates expectations have repriced higher, with an implied 100% probability of an ECB rate hike by December 2026.

Source: Bloomberg. Data as of 27/02/2026

While there may well be an inflationary impact for Europe (and others) in case of a prolonged war and/or closure of the Strait of Hormuz, economic growth would also likely suffer.

In that scenario – and especially after the disastrous experience of the ECB hikes of 2011 – I think growth concerns would prevail, and so the implied probability highlighted above seems way too high.

While this observation does not automatically lead to any obvious changes to make in portfolios today, perhaps it can help focus the attention for what feels like an inevitably noisy next phase of this current market environment.

Mood music: Leonard Cohen – You Want It Darker

By popular demand, here is the One week / One topic playlist