- Markets Mirage

- Posts

- One week / one topic: Fog of war

One week / one topic: Fog of war

So many different suns

Stefano Amato

March 23, 2026

What happened?

There is a regional war in the Middle East, and we don’t know why it was started, what’s next, when it’s going to end or how.

To further complicate the picture, the historical precedents of Trump’s sudden and unilateral climbdowns keep hopes alive that this might also somehow come to an end soon.

Meanwhile, markets are attempting to price in an appropriate risk premium. Good luck with that…

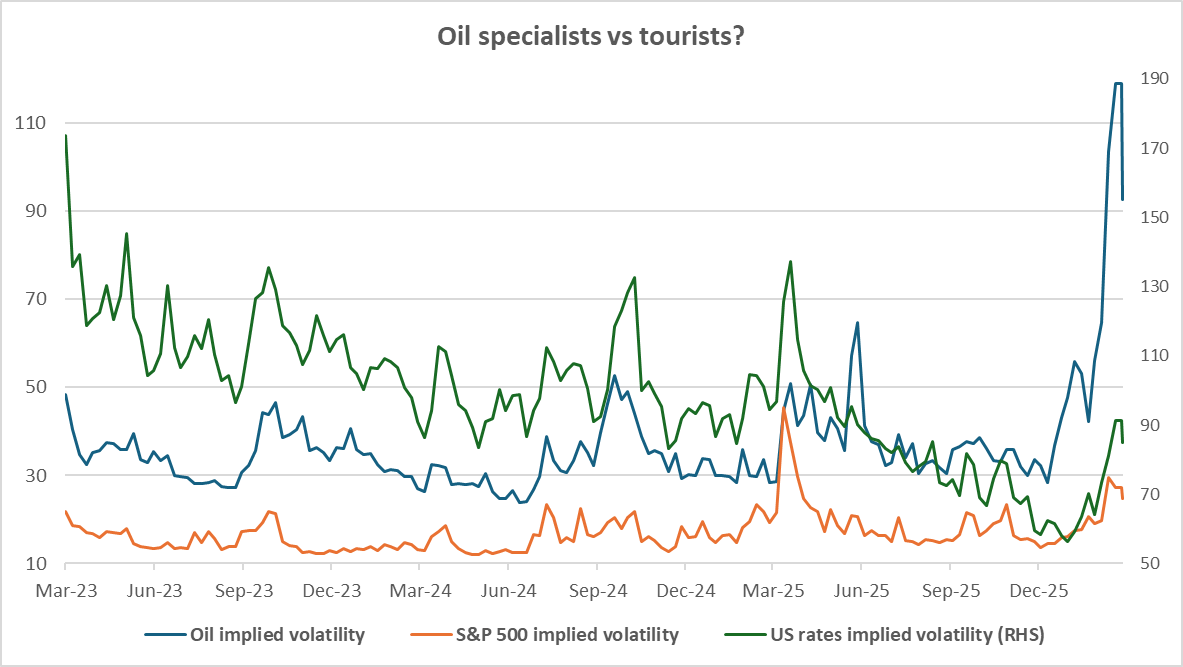

For now – in short – the oil market is much more worried than either equities or rates.

Source: Bloomberg. Data as of 20/03/2026

Recent attacks on energy infrastructure clearly justify worries about prolonged disruption and long lead times before production can return to anything resembling normality.

At the same time, financial assets like equities and bonds can count on central banks as the ultimate backstop in their role of lender of last resort.

Put simply, you can print money when needed – but not commodities.

Source: Bloomberg. Data as of 20/03/2026

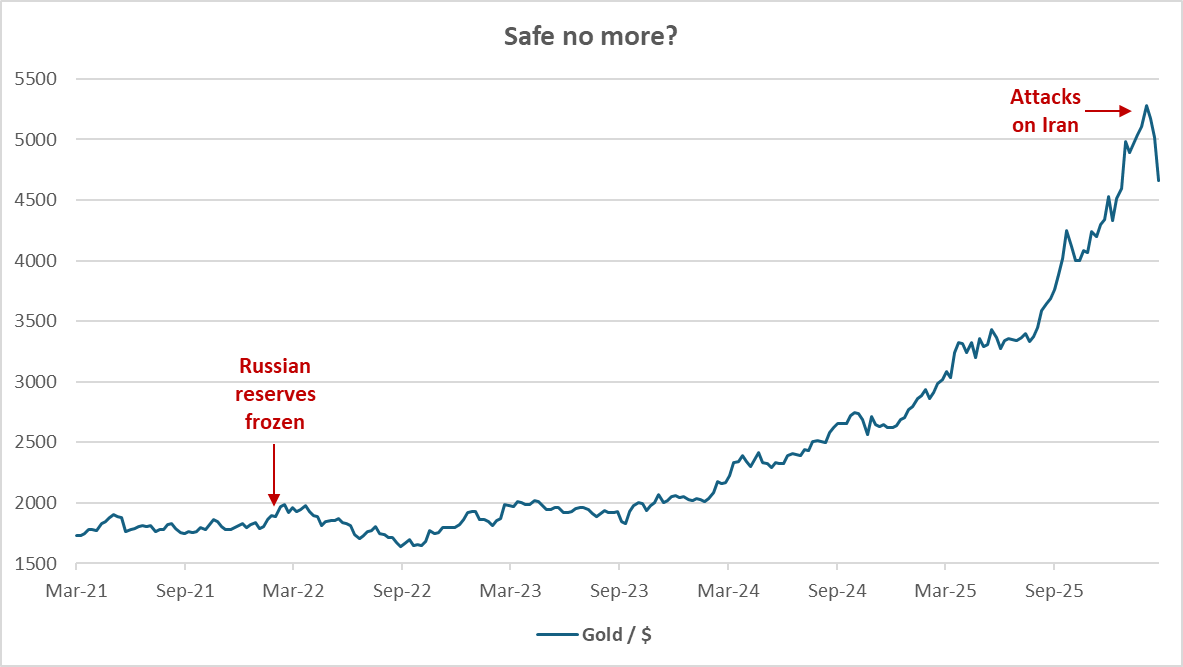

Oh, and if you were thinking that this is exactly the scenario that would send gold prices to the moon – war, oil blockade, rising volatility – well… think again.

Since Europe froze Russian reserves in 2022, surplus countries have directed more and more of their excess savings into gold.

Speculators jumped in, and the transformation from safe haven to risk asset is now seemingly complete, judging from the latest price action.

Source: Bloomberg. Data as of 20/03/2026. Past performance is not a guide to future performance.

What should we do in the meantime then, while we wait for this unpredictable source of uncertainty to be somehow resolved?

Our observations

Fundamentals: While the recent equity drawdowns have inevitably brought down valuations, not much is obviously cheap.

Plus, how will corporate earnings be affected is anyone’s guess at this stage.

Price action: 15+ years conditioning to always ‘buy the dip’ inevitably inform recent price movements.

Whether this will work once again or not remains to be seen…

Investor beliefs: The lack of outright panic might signal that markets think that, after all, there is a deal to be done.

Maybe… Hopefully? But then again, beware of unintended consequences.

Source: Bloomberg. Data as of 20/03/2026

So what?

Echoing Charlie Munger’s claim that “Diversification is for those who don’t know anything” and given the current environment, we have indeed reduced idiosyncratic risk across portfolios.

Within equities, we have tempered our preference for Japanese and Emerging Markets while retaining a tilt due to more favorable valuations.

On the fixed income side, we have a diversified exposure across US, UK and German government bonds which is varied between nominal and inflation-linked bonds, and expressed across different maturities as well.

Furthermore, we maintain a hedged exposure to short maturity crossover credit and a regionally diversified exposure to Emerging Markets bonds as well, where we express a preference for LatAm issuers.

Decision-making under uncertainty is the name of the game in investing, but – in times like these – we definitely want to pick our spots.

Mood music: Dire Straits – Brothers in Arms

By popular demand, here is the One week / One topic playlist