- Markets Mirage

- Posts

- One week / one topic: Carnival

One week / one topic: Carnival

Obá–obá–obá

Stefano Amato

February 09, 2026

What happened?

Since this coming Friday marks the official start of the 2026 Rio de Janeiro carnival (never been), it might be a good time to examine one of our highest-conviction positions: Brazil.

On the assumption that ‘country risk’ tends to trump anything else when it comes to emerging markets (EM) – i.e. equities, bonds and currencies move together much more than in so-called ‘developed markets’ (DM) – it makes sense to assess the three main local asset classes at the same time.

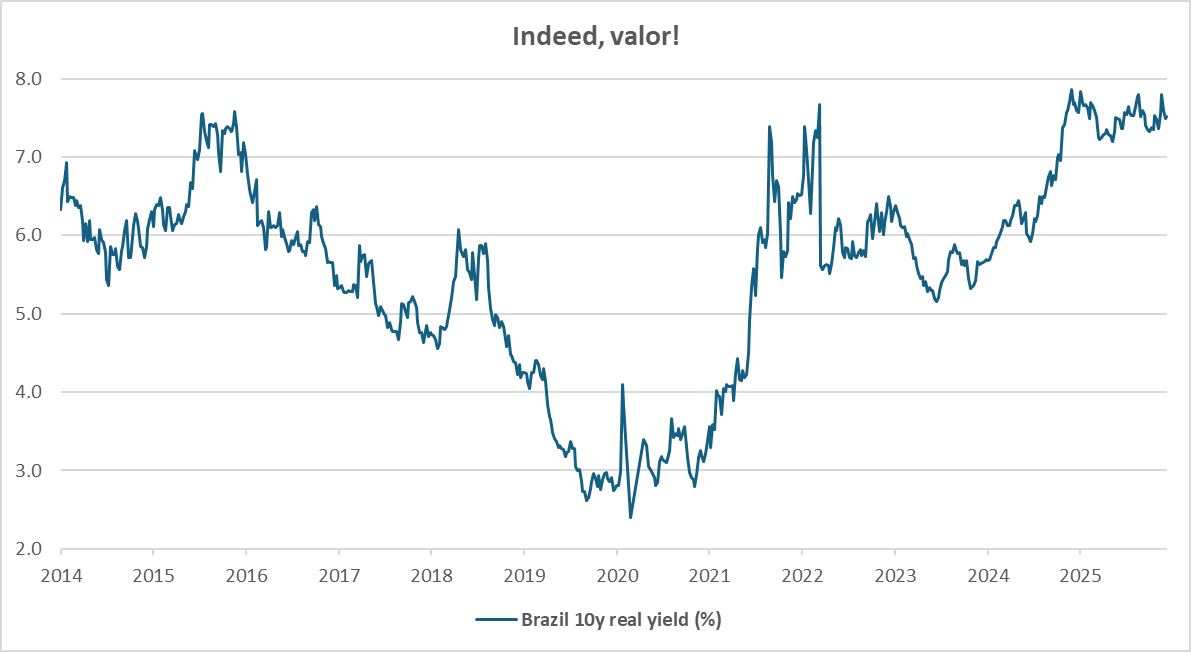

Starting from FX, the Brazilian Real can boost strong real yields, ‘fair valuations’ and an improving cyclical backdrop.

While spot returns will likely retain cyclical sensitivity and therefore remain vulnerable to decreased risk appetite, 10y real yields at the 95th percentile are hard to argue with.

Past performance is not a guide to future performance. Data as of 06/02/2026

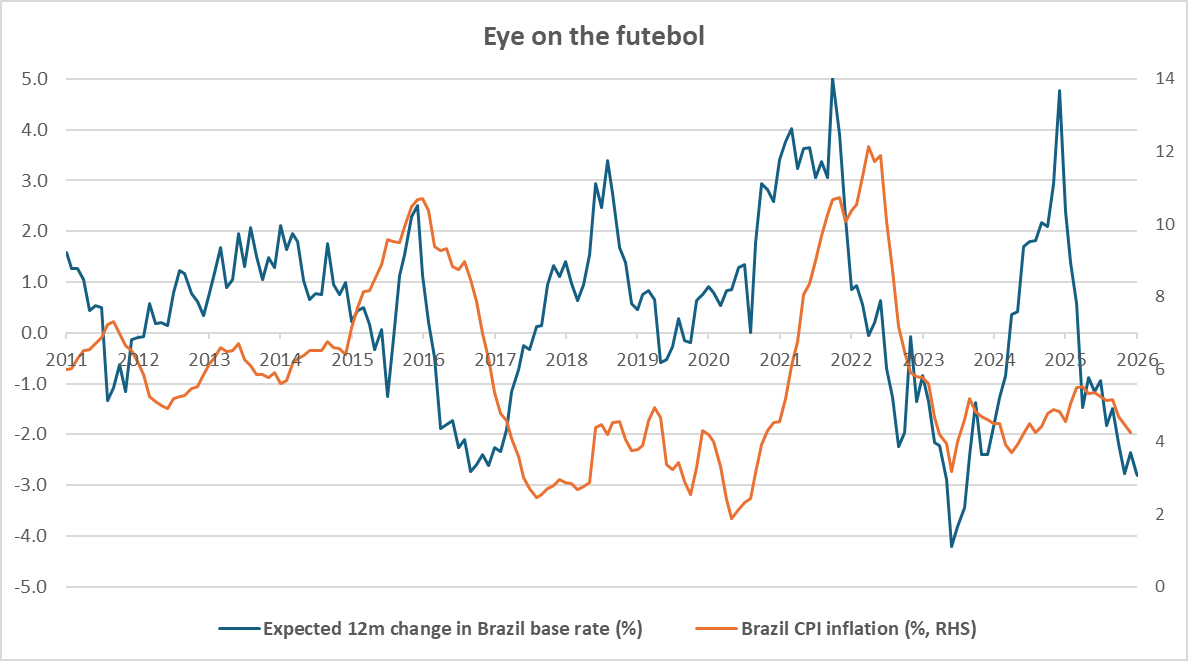

Local government bonds also look attractive in my view given high current yields (~90th percentile over the last 20 years), and the very fact that high real rates provide cushion and room for policy easing.

While the market is indeed already pricing in deep cuts, local policymakers have earned their stripes by managing the last cycle quite well.

Indeed, senior central bank officials keep stating that fiscal sustainability remains a big concern, it has to be taken into account in setting monetary policy and extra caution is needed ahead of the October presidential elections.

Data as of 06/02/2026

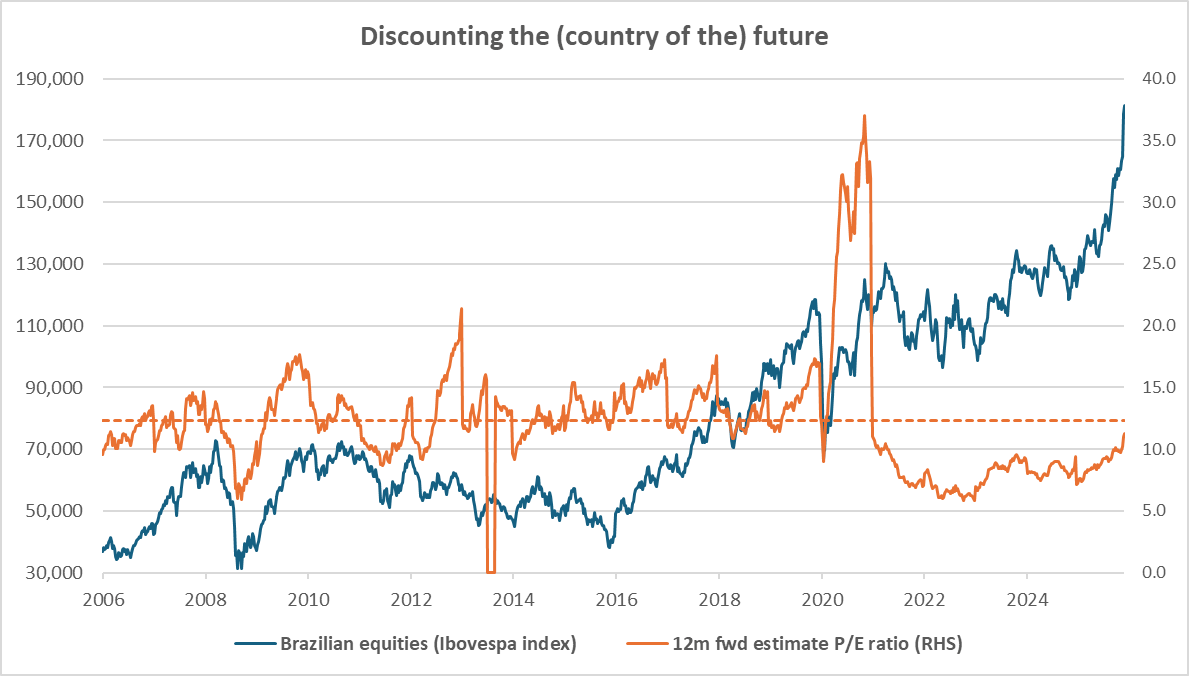

Finally, Brazilian equities – even if they have rallied ~40% over the last six months – remain relatively inexpensive.

Despite positive earnings revisions, valuations are less demanding than for broad EM indices and might continue to benefit from macro tailwinds in the form of a weaker US dollar and higher commodity prices.

Past performance is not a guide to future performance. Data as of 06/02/2026

However, I do believe that we inhabit a strange and foreign land where so-called fundamentals are questioned more and more, and where narratives can barely garner any attention before the next news cycle takes over.

In that context, what should we do about our overall exposure to Brazilian assets?

Our observations

Fundamentals: Between now and the October elections, there is a very high chance of political noise swamping any fundamentals-based considerations – at least in the short term. That said, such developments might also offer attractive entry points…

Price action: While recent rallies in equities and the Real have been hard to miss, real rates remain at very attractive levels.

Investor beliefs: Investors have overall warmed to emerging markets after the recent strong performance and there could well be much more to go from here, but fickle preferences remain a concern should there be any bouts of volatility.

So what?

The traditional axiom about EM ‘country risk’ would state that, in a crisis, local assets all go down at the same time.

Furthermore, should there be a sizeable global slowdown or crisis, the ‘risk-on’ character of Brazilian assets would also engender vulnerability.

But would this be true on a relative basis? I.e. would you be penalized more than if you owned similar positions in global assets?

In the first scenario (a Brazil-specific crisis), I would normally answer ‘yes’.

However, if the most likely source of country-specific turmoil is the upcoming presidential election in October, the experience of the last few years should have taught us all about the radical unpredictability of political outcomes and their market impact.

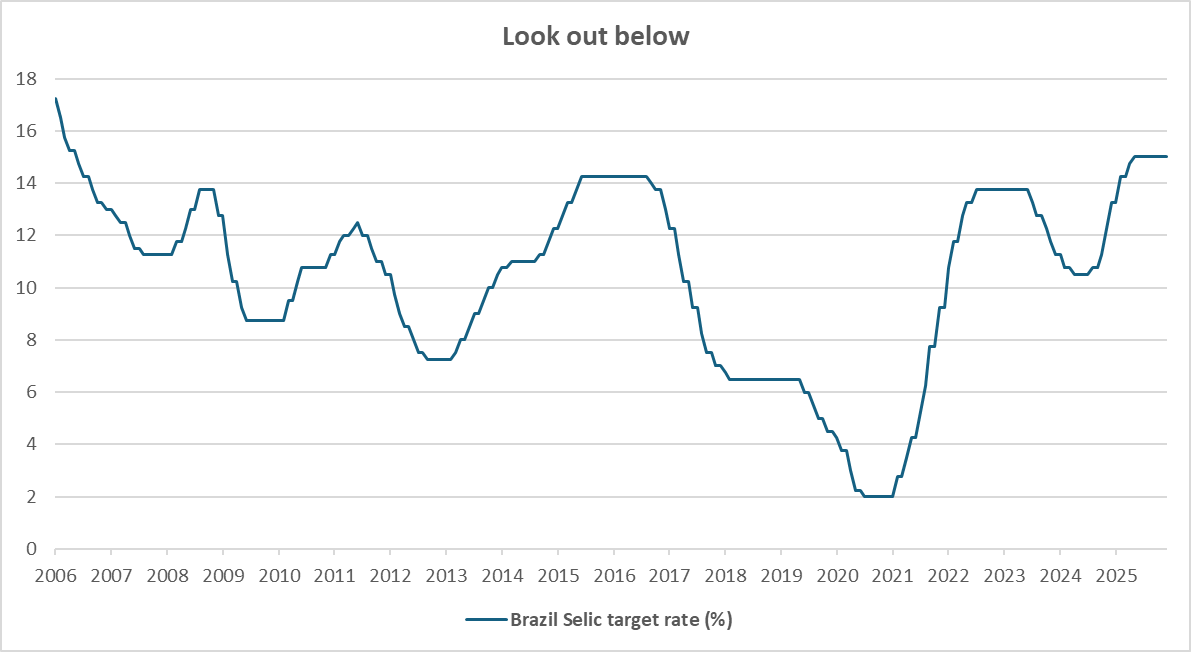

Furthermore, the Brazilian central bank might counteract any shocks by slashing rates to the tune of several hundred basis points (they currently sit at 15%).

With that in mind, I’d lean towards changing my answer above from ‘yes’ to ‘maybe’…

Data as of 06/02/2026

And what about the ‘global crisis’ scenario? Would Brazilian FX, local bonds and equities underperform developed markets equivalents?

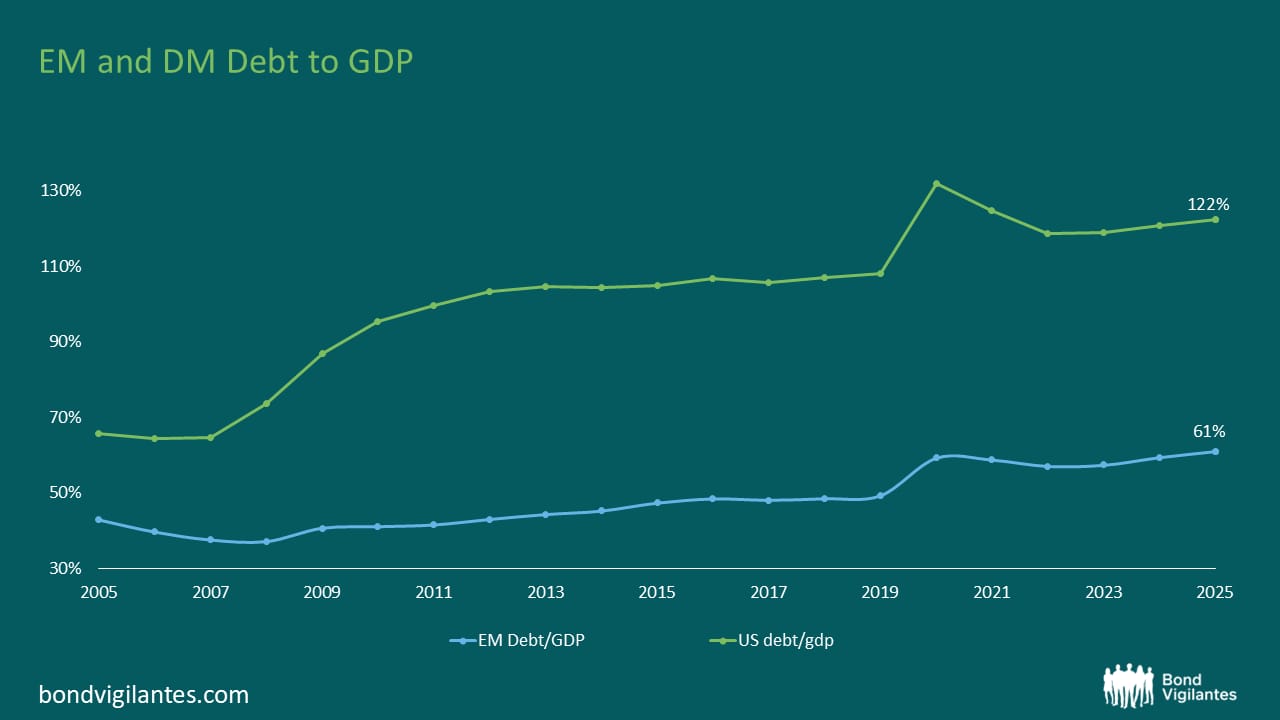

Markets still price a sizable risk premium for EM assets despite what are in many cases stronger fundamentals in terms of economic growth, fiscal sustainability or corporate earnings dynamics.

In other words, EM assets trade at a discount vs developed markets based on a set of beliefs and recency bias.

These beliefs would only be really tested in a proper crisis, but 1) we might not get one for a long time (who knows?), and 2) it is all relative, since many developed countries have been working hard to dismantle their own fiscal and monetary credibility.

On balance, we then retain conviction in our Brazilian positions in the context of a highly diversified portfolio.

Put differently, we still see good potential here – but we are not betting the fazenda on it.

Mood music: Al Jarreau – Mas Que Nada – Live 1993 Version

By popular demand, here is the One week / One topic playlist